CFPB Workforce Cuts: What Fintech Startups Must Do Now

The CFPB Is Shrinking. The Compliance Obligation Is Not.

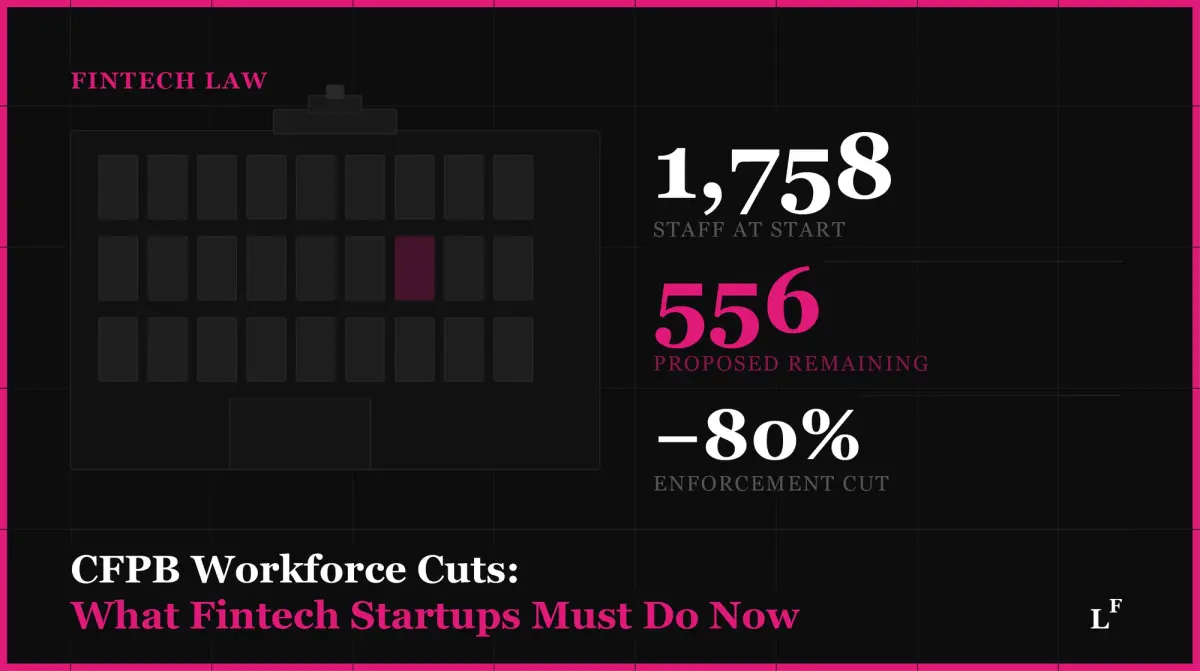

On April 1, 2026, the Justice Department filed court documents revealing the Trump administration's revised plan to cut the Consumer Financial Protection Bureau's workforce by approximately two-thirds — down from an earlier proposal to eliminate nearly 90% of staff. Under the new plan, the bureau's headcount would fall from roughly 1,174 current employees to 556, fewer than a third of the 1,758 on staff when President Trump took office. The reduction targets supervision and enforcement specifically: the Division of Supervision would lose 85% of its positions — from 523 to 77 — and enforcement would be cut 80%, from 254 to just 50 attorneys and staff. (American Bazaar; ABA Banking Journal; PYMNTS)

The filing is not a resolution. It is a negotiating position in ongoing litigation — NTEU v. Vought — currently before the U.S. Court of Appeals for the D.C. Circuit, where judges have appeared skeptical of the administration's earlier arguments. The current stay blocking the workforce reduction remains in effect until the court rules. But the direction is unmistakable: the CFPB as a supervisory and enforcement institution is being deliberately hollowed out. (AFR)

For fintech startups and digital asset companies operating under CFPB jurisdiction, the instinct to exhale is understandable. Resist it.

What the Workforce Reduction Actually Changes — and What It Does Not

Here’s the part most coverage is missing. The CFPB's statutory authority does not shrink when its headcount does. The Consumer Financial Protection Act, the Truth in Lending Act, the Electronic Fund Transfer Act, and the rules governing money transmitter activity at the federal level remain fully in force regardless of how many examiners are on payroll. What changes is enforcement capacity and examination frequency — not legal exposure.

The administration's own court filing acknowledged this: the revised reduction-in-force plan was structured to show that the bureau can still "meet its statutory obligations" at 556 employees — precisely because those obligations do not disappear with the staff. (ABA Banking Journal)

Two dynamics follow from this.

- State attorneys general and state financial regulators are already filling the vacuum. Acting Director Russell Vought stated last year that the CFPB would cede supervision and enforcement to state regulators — a position that New York, California, and Illinois have treated as an invitation. Each has signaled intent to expand consumer financial protection enforcement at the state level. A fintech startup that treated CFPB oversight as its primary compliance concern now faces a patchwork of state regulators, each with independent authority and distinct procedural expectations.

- Private litigation risk increases when agency enforcement decreases. Plaintiffs' attorneys watch enforcement gaps closely. A company whose terms of service or privacy policy contains provisions that a fully staffed CFPB might have flagged in an examination is now more likely to see those provisions tested in a class action than in a consent order. The GAO's January 2026 report on the CFPB's reorganization documented that the bureau has already withdrawn from 56 enforcement actions — resolving only seven and continuing just nine. (CFS Law Monitor)

The Distinction That Matters: Supervision Gap vs. Liability Gap

There is a critical distinction that fintech founders and their counsel must draw right now. A supervision gap — fewer examiners, slower examination cycles, reduced enforcement actions — is real and measurable. A liability gap does not exist.

The legal obligations that attach to consumer-facing financial products do not pause because the agency charged with enforcing them is understaffed. This distinction matters most for companies operating at the intersection of cryptocurrency regulation and consumer finance. Digital asset platforms that offer lending, payments, or yield products to retail customers carry CFPB-adjacent obligations whether or not the Bureau has the capacity to examine them. The same applies to buy-now-pay-later providers, earned wage access companies, and any fintech startup offering credit or payment products under a bank partnership model.

Tokenization of real-world assets does not create a regulatory exemption. If the underlying product touches consumer credit or payments, the compliance framework must reflect that — regardless of what the CFPB's organizational chart looks like.

What Fintech Startups Should Do Before the Dust Settles

- Audit your consumer-facing documents now. Your terms of service, privacy policy, and any consumer disclosures should be reviewed against current CFPB rules and applicable state consumer protection statutes. The companies most exposed in a state enforcement environment are those whose documents were drafted for a federal-primary world.

- Map your state money transmitter obligations. If your product involves moving money — including stablecoin transfers, crypto-to-fiat conversions, or digital asset payments — your money transmitter licensing posture needs a fresh review. State regulators do not need the CFPB to act. Several states have already initiated enforcement actions against unlicensed digital asset payment providers independent of any federal coordination.

- Don’t treat the litigation pause as a compliance holiday. The appeals court proceedings are ongoing. The Bureau's authority could be clarified, expanded, or constrained by judicial decision on a timeline no one can predict. Compliance programs built around the assumption that the CFPB is permanently diminished are built on a fragile foundation.

- Assess your SEC enforcement exposure separately. For companies in the digital assets space, CFPB uncertainty does not reduce SEC enforcement risk. The two agencies operate on independent tracks. The SEC-CFTC joint interpretive release issued on March 17, 2026 makes clear that digital asset oversight is being strengthened, not weakened, at the federal level. A fintech startup that offers tokenized securities or investment products faces SEC scrutiny that is entirely unaffected by CFPB staffing levels.

Key Takeaways

- The CFPB's statutory authority survives its workforce reduction. Legal obligations under federal consumer financial protection law remain in force regardless of the Bureau's examination capacity or staffing levels.

- State regulators are the more immediate enforcement risk for most fintech startups. New York, California, and Illinois have each signaled intent to expand consumer financial protection enforcement, creating a multi-jurisdictional compliance obligation that a CFPB-focused program won’t address.

- Terms of service and privacy policy documents are now front-line litigation targets. With reduced agency enforcement, plaintiffs' attorneys will test consumer-facing provisions directly. Documents that have not been reviewed recently carry real exposure.

- Money transmitter licensing gaps do not close because the CFPB is smaller. State money transmitter regulators operate independently and have demonstrated willingness to act against digital asset and fintech companies without federal coordination.

- Cryptocurrency regulation and digital asset compliance obligations are unaffected by CFPB developments. SEC enforcement priorities, state securities regulators, and FinCEN obligations continue on their own tracks. A CFPB-focused compliance review is not a substitute for a full regulatory audit.

The Real Question Isn’t Whether the CFPB Survives. It's Whether Your Compliance Program Does.

The CFPB's workforce reduction is a significant institutional development. It is not a compliance reprieve. The companies that will be best positioned when the regulatory picture clarifies — whether that means a reconstituted Bureau, aggressive state enforcement, or expanded private litigation — are those that used this period to build compliance programs that do not depend on any single agency's capacity to enforce them.

FinTech Law works with fintech startups, digital asset companies, and AI legal tech platforms to build compliance infrastructure that holds up across regulatory environments. If your firm is operating in consumer finance, payments, or digital assets and has not reviewed its compliance posture in light of recent CFPB developments, we would welcome the conversation.

Contact us or subscribe to our newsletter for ongoing analysis as this situation develops.

Disclaimer: This blog post is for informational purposes only and does not constitute legal advice. No attorney-client relationship is formed by reading this content. If you need legal advice, please contact a qualified attorney.