Trump Administration Fast-Tracks Erebor Bank Approval: What Crypto & Fintech Startups Need to Know

Palmer Luckey and Peter Thiel's digital bank signals a new era for crypto banking, stablecoins, and defense tech financing

The OCC's unprecedented four-month approval could end "de-banking" for crypto firms—but political controversy raises questions about favoritism and systemic risk.

By Bo Howell (using Claude Sonnet 4.5 and Grok 4 Fast)

The Office of the Comptroller of the Currency (OCC) has granted preliminary conditional approval to Erebor Bank, a digital-first institution co-founded by defense tech entrepreneur Palmer Luckey (Oculus, Anduril) and backed by venture capitalist Peter Thiel's Founders Fund. Announced on October 15, 2025, this lightning-fast approval—just four months after the June 11 application—shatters typical banking charter timelines and signals the Trump administration's dramatically more crypto-friendly regulatory approach.

For fintech and crypto startups still reeling from Silicon Valley Bank's 2023 collapse, Erebor promises specialized services that traditional banks refuse: stablecoin operations, crypto-collateralized lending, and banking infrastructure designed for AI, defense, and digital asset companies. But with Senator Elizabeth Warren condemning the approval as "crony capitalism" and critics warning of another taxpayer-funded bailout, the controversy is just beginning.

Key Facts at a Glance:

- Application to Approval: 4 months (June 11 - October 15, 2025) vs. typical 12-18 months

- Capital Raised: $275 million at $2B+ valuation

- Founders: Palmer Luckey (Anduril), Joe Lonsdale (Palantir), backed by Peter Thiel

- Focus: Crypto, AI, defense, manufacturing companies + stablecoins

- What's Next: FDIC approval (9-10 months typical), Federal Reserve membership

- Capital Requirement: 12% Tier 1 Leverage ratio (double typical requirements)

The Silicon Valley Bank Void: Why Tech Startups Need Erebor Now

Silicon Valley Bank's collapse in March 2023 left a critical gap in the banking ecosystem. SVB served nearly 50% of all U.S. venture capital-backed technology and healthcare companies, providing specialized banking services that traditional institutions typically avoid.

What Went Wrong: Rising interest rates in 2022 decimated SVB's bond portfolio while tech startups increasingly withdrew deposits as venture capital funding dried up. Within 48 hours, SVB went from solvent to insolvent—the second-largest bank failure in U.S. history after Washington Mutual in 2008.

The Damage:

- Assets Frozen: $175 billion in deposits, affecting companies from Roku to Rocket Labs

- Startup Disruption: 90% of venture capital firms reported impacts on portfolio companies

- The Lesson: Concentration risk kills—both for banks and their clients

Erebor Bank positions itself as SVB's successor, but with crucial differences: digital-only from day one, crypto-native infrastructure, and substantially higher capital requirements (12% Tier 1 Leverage vs. standard 4-6%). The bank explicitly targets the "innovation economy"—AI, defense, crypto, and manufacturing companies that struggle to find banking partners willing to understand their business models.

The Power Players Behind Erebor: Luckey, Thiel, and the Tolkien Connection

Palmer Luckey, who founded Oculus VR before selling it to Meta and now leads defense technology firm Anduril Industries, co-founded Erebor with Joe Lonsdale, co-founder of data analytics giant Palantir Technologies. The bank is backed by Peter Thiel's Founders Fund, along with 8VC and Haun Ventures, raising $275 million at a valuation exceeding $2 billion.

The Leadership Team:

- Co-CEOs: Owen Rapaport and Jacob Hirshman (banking and regulatory experience)

- Notable Connection: Adam Cohen, formerly of Skadden and Erebor's OCC application lawyer, joined the OCC as chief counsel to Comptroller Jonathan Gould in August 2025

The Tolkien Connection: Like Anduril and Palantir, Erebor's name comes from J.R.R. Tolkien's works. In "The Hobbit," Erebor is the mountain fortress and kingdom of the dwarves—a name suggesting security, treasure management, and defensive strength that the founders hope projects confidence for their banking venture.

The Political Dimension: These GOP megadonors' connections to the Trump administration extend beyond campaign contributions. Palantir and Anduril have secured billions in federal contracts for data analytics, surveillance, and defense technologies. Luckey alone contributed over $1 million to Republican causes in 2024, raising questions about whether political influence affected the regulatory process.

The Unprecedented Four-Month Approval: Innovation or Favoritism?

The Timeline That Raised Eyebrows:

- Typical Process: 12-18 months for de novo bank charter applications

- Erebor's Experience: 4 months (June 11 - October 15, 2025)

- The 120-Day Standard: OCC guidelines target 120 days, but this is "generally honored only in the breach," according to banking experts

The Controversial Memo: According to Business Insider, Erebor's fundraising documents told prospective investors that the bank expected approval in "less than six months," explicitly stating: "Palmer's political network will get this done." The memo also touted an Erebor co-founder's "unique connectivity to banking regulators," including Comptroller Gould.

The Political Context:

- Luckey donated $1 million+ to Republican causes in 2024

- Thiel, Luckey, and Lonsdale are major Trump supporters

- Their companies (Palantir, Anduril) hold billions in Trump administration contracts

- Adam Cohen's move from Erebor's legal team to OCC chief counsel raised conflict-of-interest concerns

The OCC's Response: Comptroller Jonathan Gould defended the approval, stating: "I am committed to a dynamic and diverse federal banking system, and our decision today is a first but important step in living up to that commitment. Today's decision is also proof that the OCC under my leadership does not impose blanket barriers to banks that want to engage in digital asset activities."

The OCC emphasized applying "the same rigorous review and standards" to all charter applications, but the dramatically compressed timeline compared to historical norms has intensified scrutiny.

What Services Will Erebor Provide: Crypto Meets Traditional Banking

Erebor will operate as a digital-only national bank headquartered in Columbus, Ohio, with a secondary office in New York. No physical branches—nationwide service via web and mobile platforms.

Target Market: Technology companies focused on virtual currencies, artificial intelligence, defense, and manufacturing, plus payment service providers, investment funds, trading firms (including registered investment advisers, broker-dealers, and futures commission merchants).

Digital Asset Integration: The Crypto-First Difference

Stablecoin Operations

- Core mechanism for low-cost transactions

- Acquired stealth-mode crypto startup Atticus for infrastructure integration

- Targets share of $312 billion stablecoin market (2025)

- Potential competitor to Anchorage Digital for issuance and custody

Crypto-Collateralized Lending

- Loans backed by cryptocurrency held on balance sheet

- Provides liquidity for crypto miners, market makers, AI firms

- Unlocks capital from digital assets without liquidation

Operational Cryptocurrency Holdings

- ~$1 million in cryptocurrency for operational use

- Pay transaction fees on Ethereum and connected blockchains

- OCC explicitly approved this request in conditional approval

Innovative Asset Lending

- Loans against graphics processing units (GPUs)

- AI hardware and specialized equipment financing

- Assets that traditional banks struggle to value or refuse to accept

Traditional Banking Services

- Business Deposit Accounts: FDIC-insured (pending approval)

- Commercial Lending: Lines of credit, term loans

- Treasury Management: Cash management, account services

- Payment Processing: ACH, wire transfers, card programs

- International Services: Banking access for global tech firms seeking U.S. rails

Regulatory Requirements and Conditions

While Erebor has received preliminary conditional approval, it cannot open for business until it satisfies numerous regulatory requirements. These conditions demonstrate the OCC's attempt to mitigate risks associated with the innovative business model.

Capital Requirements

The OCC has imposed strict capital requirements on Erebor Bank. The institution must maintain a minimum 12% Tier 1 Leverage ratio for its first three years of operation. This substantially exceeds the standard minimum capital requirements for national banks, reflecting the OCC's recognition that Erebor's activities may carry heightened risks.

The bank has raised $275 million in capital to support its operations, demonstrating significant financial backing from its investor group. This capital cushion should provide a buffer against potential losses as the bank establishes its business model.

FDIC Insurance Requirement

Before opening, Erebor must obtain approval from the Federal Deposit Insurance Corporation (FDIC) for deposit insurance. This process typically takes nine to ten months and requires separate application and approval procedures. The FDIC conducts its own review of the bank's safety and soundness, business plan, and management team.

FDIC approval is not guaranteed, and the agency has historically taken a cautious approach to innovative banking models, particularly those involving digital assets. The FDIC's decision will be closely watched as a signal of whether federal regulators are aligned in their willingness to support crypto-friendly banking.

Management Approval

The OCC must provide non-objection to Erebor's senior executive team before the bank can commence operations. This gives regulators authority to reject management candidates who lack appropriate qualifications or experience. The OCC retains the right to object to the hiring of any officer or appointment of any director for two years after the bank opens for business.

Federal Reserve Membership

Erebor must also apply to the Federal Reserve stock, which is required for all national banks as they must be members of the Federal Reserve System. This application must be submitted at least four weeks before the bank's projected opening date and requires Federal Reserve approval.

Operational Agreements

The OCC may require Erebor to enter into an operating agreement containing substantive charter conditions specific to its business model. These agreements typically include provisions for risk management, compliance programs, capital maintenance, and restrictions on activities or growth until certain benchmarks are met.

Political Controversy and Concerns

The Erebor approval has generated significant political controversy, with critics arguing that it represents favoritism toward politically connected billionaires and may expose taxpayers to future bailout risks.

Senator Warren's Opposition

Senator Elizabeth Warren (D-Mass.), the ranking member of the Senate Banking Committee, issued a strongly worded statement condemning the approval. "President Trump's billionaire buddies Peter Thiel and Palmer Luckey just received approval from the OCC to launch a new bank that will cater to the financial whims of Silicon Valley billionaires," Warren said. "In a free market, credit flows fairly to businesses because they can use the money productively, not to the President's cronies because of their political connections."

Warren characterized the decision as "a textbook example of crony capitalism" and warned that "Trump's financial regulators just fast-tracked an approval of this risky venture that could set up another bailout funded by American taxpayers and destabilize our banking system."

These concerns reflect broader Democratic skepticism about the Trump administration's approach to cryptocurrency regulation and the potential for conflicts of interest given Trump's own investments in digital assets.

Political Connections

The founders' political connections extend beyond campaign contributions. Palantir, co-founded by Thiel and Lonsdale, has received billions of dollars in contracts from the Trump administration for data analytics and surveillance technologies. Similarly, Luckey's Anduril Industries has secured multibillion-dollar deals to develop military tools and border security systems for the federal government.

These business relationships raise questions about whether favorable regulatory treatment represents a quid pro quo for political support and government contracts. While the OCC insists it followed standard procedures, the appearance of preferential treatment has damaged public confidence in the regulatory process.

Systemic Risk Considerations

Beyond political concerns, some financial experts worry about the systemic risks posed by a crypto-friendly bank serving high-risk technology companies. The SVB collapse demonstrated how quickly a bank with concentrated exposure to a single sector can fail when that sector faces headwinds.

Erebor's focus on virtual currencies, AI companies, and defense contractors creates similar concentration risk. If cryptocurrency markets experience significant turmoil or if technology startup funding dries up again, Erebor could face rapid deposit withdrawals, which would strain its liquidity.

However, supporters argue that Erebor's digital-only model, higher capital requirements, and focus on stablecoins and crypto-collateralized lending actually reduce some of these risks compared to SVB's traditional bond-heavy portfolio. The debate over whether Erebor represents innovation or recklessness will likely continue as the bank moves toward opening.

What This Means for Fintech Companies

The Erebor approval signals important developments for financial technology companies and digital asset businesses seeking banking relationships.

Access to Traditional Banking

For years, cryptocurrency companies and fintech startups have struggled to obtain and maintain banking relationships. Traditional banks often view these businesses as too risky or compliance-intensive, leading to account closures and limited service options. This phenomenon, known as "de-banking," has constrained growth in the digital asset sector.

Erebor's approval suggests that federally regulated banking institutions can serve crypto businesses if they implement appropriate risk management frameworks. This could encourage other banks to reconsider their approach to digital asset clients or inspire additional charter applications for crypto-friendly banks.

Stablecoin Infrastructure

Erebor's planned stablecoin operations could provide critical infrastructure for the growing stablecoin market, which reached approximately $312 billion in capitalization in 2025. If Erebor successfully implements stablecoin issuance and custody services, it may directly compete with existing players like Anchorage Digital and offer additional options for businesses seeking stablecoin solutions.

The bank's approach to integrating stablecoins with traditional banking services could serve as a model for how digital and traditional finance can converge, potentially accelerating mainstream adoption of blockchain-based payment systems.

Lending Against Digital Assets

Crypto-collateralized lending has historically been provided primarily by non-bank lenders or overseas institutions. Having a federally regulated U.S. bank offer these products brings several advantages, including potentially lower interest rates, FDIC-insured deposits for borrowers holding deposit accounts, and regulatory oversight that may attract more conservative institutional participants.

For businesses that hold cryptocurrency or specialized technology assets, Erebor's lending programs could unlock liquidity that would otherwise be inaccessible through traditional banks. This particularly benefits crypto miners, market makers, and AI infrastructure companies with substantial equipment investments.

Regulatory Template

Perhaps most significantly, Erebor's approval process and the conditions imposed by the OCC may serve as a template for future fintech charter applications. Other entrepreneurs and investors will study Erebor's business plan, capital structure, and compliance framework to understand what regulators expect from digital asset banks.

The OCC's willingness to approve a crypto-focused bank charter, despite political controversy, suggests that the current regulatory environment may be more receptive to financial innovation than in previous years. This could encourage additional charter applications and accelerate the development of a specialized banking sector for technology companies.

Legal and Compliance Considerations

Companies considering banking with Erebor or pursuing similar charter strategies should understand several key legal and compliance issues.

Regulatory Dual-Track Approach

While the OCC has granted preliminary approval, final authorization requires both FDIC insurance approval and satisfaction of all conditional requirements. This dual-track approach means that OCC approval alone does not guarantee that Erebor will open. Fintech companies should not assume banking services will be available until all regulatory hurdles are cleared.

The FDIC has historically taken a more conservative stance on digital asset activities than the OCC, particularly under previous leadership. Its decision on Erebor's insurance application will signal whether there is true regulatory alignment on crypto banking or whether conflicts between agencies may constrain such institutions.

Enhanced Due Diligence Requirements

Banks engaged in digital asset activities typically face enhanced due diligence and compliance requirements. Erebor will likely implement strict know-your-customer (KYC) and anti-money laundering (AML) procedures that may exceed those of traditional banks.

Businesses seeking to bank with Erebor should prepare for comprehensive documentation requirements, including detailed information about beneficial ownership, source of funds, business models, and transaction patterns. Companies with complex ownership structures or operations in high-risk jurisdictions may face additional scrutiny.

BSA/AML Compliance for Crypto Activities

The Bank Secrecy Act and anti-money laundering regulations apply with particular force to cryptocurrency-related activities. Erebor must implement robust transaction monitoring systems, suspicious activity reporting procedures, and currency transaction reporting protocols specifically designed for digital assets.

This compliance infrastructure will likely be more sophisticated than what many crypto businesses currently maintain, potentially requiring clients to upgrade their own compliance programs to meet the bank's standards. Companies should view this as an opportunity to strengthen their regulatory posture rather than simply as a burden.

Preemption and State Law Considerations

As a national bank, Erebor enjoys certain federal preemptions that exempt it from many state banking laws. However, not all state laws can be preempted by federal law. Laws relating to contracts, torts, debt collection, property acquisition and transfer, criminal law, and often state unfair and deceptive acts and practices (UDAP) laws continue to apply.

Fintech companies must understand that banking with a national bank does not provide complete immunity from state regulation, particularly regarding consumer protection laws and lending practices. Companies operating in multiple states must maintain compliance with applicable state laws, even when utilizing federally chartered banking services.

Resolution and Wind-Down Planning

Given the political controversy and regulatory scrutiny surrounding Erebor, the bank may face unusual pressures if it encounters financial difficulties. The OCC may impose special conditions requiring the bank to have a resolution plan in place for selling itself or winding down its operations if necessary.

Companies relying on Erebor for critical banking services should develop contingency plans for transferring relationships to alternative institutions if needed. The SVB collapse demonstrated how quickly banking relationships can be disrupted, particularly for institutions serving concentrated customer bases.

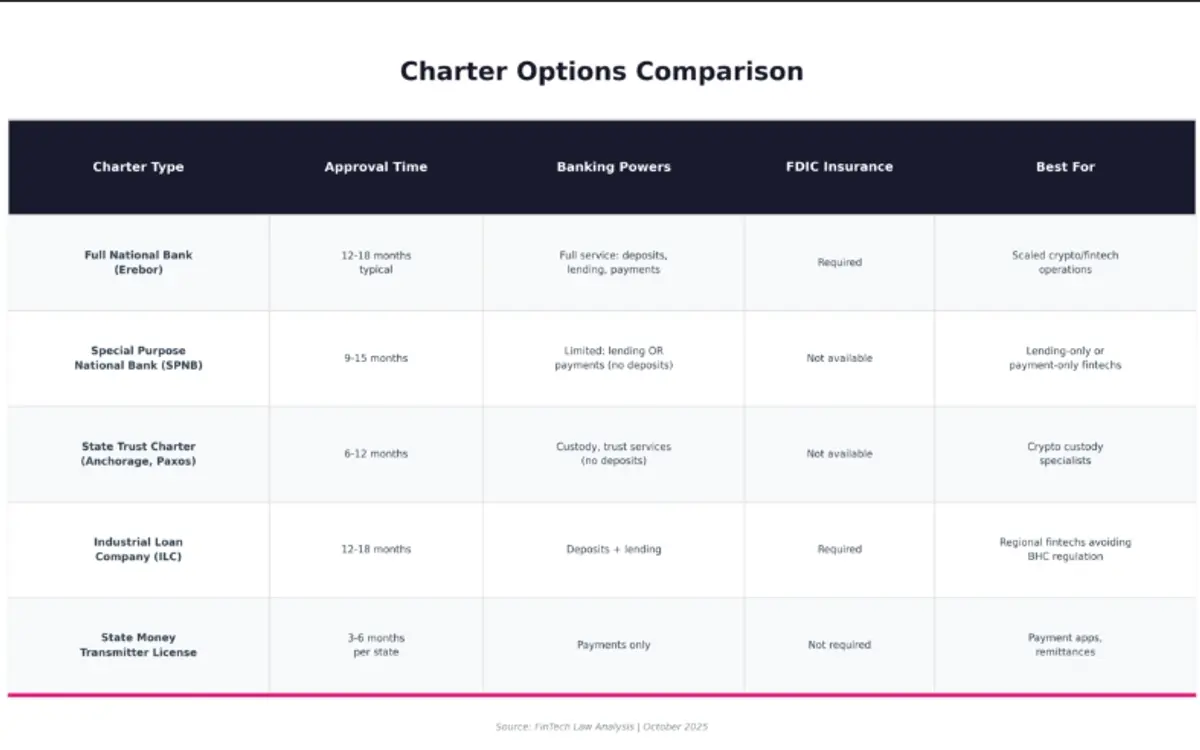

Comparison with Other Charter Approaches

Erebor's national bank charter is one of several regulatory pathways available to fintech companies. Understanding the alternatives clarifies why Erebor's founders chose this approach and the tradeoffs involved.

Why Full National Bank Charter?

Advantages for Erebor:

- Nationwide Operations: Single charter covers all 50 states

- Full Banking Powers: Deposits, lending, and payments under one roof

- Federal Preemption: Exemption from many state banking laws (but not all consumer protection laws)

- Credibility: National bank status signals regulatory oversight and stability

- Competitive Positioning: Can offer a complete banking relationship vs. limited services

The Tradeoffs:

- Higher Capital Requirements: $275M+ needed vs. $10-50M for alternatives

- Multi-Agency Approval: OCC + FDIC + Federal Reserve (vs. single state regulator)

- Enhanced Scrutiny: Federal examination vs. potentially lighter state oversight

- Longer Timeline: Even "fast" 4-month approval exceeds SPNB or state charter times

- Political Exposure: National profile attracts more attention and controversy

Special Purpose National Bank Charter

The OCC has offered special purpose national bank (SPNB) charters to fintech companies since 2018, allowing institutions to engage in limited banking activities without accepting FDIC-insured deposits. While Erebor is pursuing a full-service charter rather than an SPNB charter, the SPNB framework established important precedents for how technology companies can become federally regulated banks.

SPNB charters may be suitable for fintech companies that wish to engage in lending or payment activities without the complexity and capital requirements associated with deposit-taking. However, the lack of insured deposits limits these institutions' funding options and may make them less attractive to customers seeking the safety of FDIC insurance.

State Trust Charters

Several cryptocurrency companies, including Anchorage Digital and Paxos, have obtained state trust bank charters, particularly in states such as New York and South Dakota, which have developed frameworks for digital asset businesses. These charters allow custody and trust activities but typically do not permit deposit-taking or traditional lending.

State trust charters offer faster approval timelines and may involve less regulatory burden than national bank charters; however, they lack the nationwide operating authority and federal preemption benefits associated with national charters. Companies must balance these considerations based on their specific business models and geographic focus.

Industrial Loan Company Charters

Industrial loan companies (ILCs) are state-chartered institutions that can engage in banking activities, including accepting FDIC-insured deposits and making loans, but are exempt from bank holding company regulation. Several fintech companies have obtained ILC charters, particularly in Utah.

ILC charters offer FDIC insurance and broad banking powers, while avoiding certain regulatory requirements that apply to national banks. However, ILCs face restrictions on interstate branching and may encounter political opposition due to the regulatory gap they exploit.

Electronic Money Institution Licenses

In European jurisdictions, electronic money institution (EMI) licenses allow payment services without requiring full banking regulation. While not directly applicable in the United States, some U.S. fintech companies have obtained EMI licenses to serve European markets while maintaining separate regulatory structures domestically.

The variety of charter types reflects the complexity of fintech regulation and the need for companies to carefully evaluate which regulatory pathway best serves their business strategy and customer needs.

Strategic Implications for Tech Startups

For technology startups, Erebor's emergence presents both opportunities and strategic considerations that extend beyond simply choosing a banking partner.

Diversification of Banking Relationships

The SVB collapse taught a painful lesson about concentration risk. Companies that held all their deposits at SVB faced existential crises when the bank failed, with some unable to make payroll or continue operations. Smart startups will diversify their banking relationships across multiple institutions, regardless of how attractive any single bank's services may be.

Erebor may serve as an excellent partner for crypto-related activities or specialized lending products, but startups should also maintain deposit accounts and credit facilities with traditional banks. This diversification protects against idiosyncratic risks while allowing companies to access specialized services where they add value.

Evaluating Banking Partners

When assessing whether to bank with Erebor or any new financial institution, startups should conduct their own due diligence beyond simply relying on federal regulatory approval. Key considerations include:

Capital Adequacy: Does the bank maintain capital levels well above regulatory minimums? Erebor's $275 million capital base relative to its planned activities will be important to monitor as the bank grows.

Management Experience: Do the bank's executives possess relevant experience in banking and risk management? While Erebor's founders bring technology expertise, the institution's success will depend heavily on the capabilities of its banking professionals.

Risk Management Framework: What systems does the bank have in place to manage credit risk, operational risk, and liquidity risk? Startups should request information about the bank's risk management practices, even at a summary level.

Political and Regulatory Risk: Given Erebor's political controversy, startups should consider whether potential reputational risks or future regulatory challenges could disrupt their banking relationships.

Service Quality and Reliability: Beyond safety and soundness, does the bank provide the quality of service, technology platforms, and customer support that startups need to operate efficiently?

Strategic Use of Specialized Services

Rather than viewing Erebor as an all-purpose banking solution, tech startups should strategically leverage the bank's unique capabilities where they provide the most value:

Digital Asset Treasury Management: For startups with significant cryptocurrency holdings or stablecoin operations, Erebor may offer superior treasury management tools compared to traditional banks that are uncomfortable with digital assets.

Crypto-Collateralized Credit Lines: Startups that prefer to hold crypto rather than liquidate it may find Erebor's collateralized lending products attractive for accessing working capital while maintaining digital asset exposure.

Payment Innovation: As Erebor develops its payment infrastructure, particularly around stablecoins and blockchain-based settlement, early adopter startups may gain a competitive advantage through faster and cheaper payment processing.

AI Infrastructure Financing: Given Erebor's focus on AI companies and willingness to lend against specialized equipment, AI startups requiring significant GPU or computing infrastructure may find more flexible financing terms than at traditional banks.

Relationship Banking Benefits

While Erebor will operate digitally, its business model emphasizes deep relationships with technology clients. The bank's founders and investors bring extensive networks in venture capital, defense contracting, and technology development that may create value beyond traditional banking services.

Startups banking with Erebor may gain introductions to potential investors, customers, or strategic partners through these networks. However, companies should be realistic about such benefits and not base their banking decisions primarily on nebulous relationship value rather than concrete service quality and financial stability.

The Future of Digital Banking

Erebor's approval represents just one chapter in the ongoing evolution of digital banking and financial services regulation. Several trends will shape how this story unfolds.

Regulatory Pendulum

Banking regulation tends to swing between periods of liberalization and restriction based on economic conditions and political priorities. The current administration's support for digital asset innovation may encourage more fintech charter applications and experimental business models.

However, regulatory approaches can change quickly, particularly if financial institutions encounter problems or if political leadership shifts. The next administration or the next banking crisis could trigger a regulatory backlash that constrains digital asset banking and imposes additional restrictions.

Fintech companies and their investors should plan for this cyclical nature of regulation rather than assuming current policies will remain stable indefinitely. Building robust risk management practices and conservative capital structures helps institutions weather regulatory changes.

Traditional Bank Adaptation

Erebor's approval may pressure traditional banks to more actively serve technology and digital asset clients. If Erebor successfully captures market share from established institutions, competitive dynamics will force incumbent banks to reconsider their risk appetites and service offerings for the tech sector.

Some traditional banks may acquire fintech companies or partner with digital asset service providers to expand their capabilities. Others may lobby regulators to restrict new entrants like Erebor, arguing that existing institutions can serve these markets without the risks posed by less experienced players.

The competitive response from traditional banks will significantly influence how much market share new digital-first institutions can capture and whether they remain niche players or evolve into major financial institutions.

Stablecoin Regulation

Federal stablecoin legislation remains under consideration in Congress, with various proposals addressing reserve requirements, redemption rights, and regulatory oversight. The passage of comprehensive stablecoin regulation would provide clarity that could accelerate adoption, but might also impose constraints on how institutions like Erebor can operate in this space.

The GENIUS Act, which set new standards for stablecoin issuance, was referenced in connection with Erebor's approval timeline. Future regulatory developments in stablecoins will directly impact Erebor's business model and may influence whether other banks enter this market.

International Competition

While Erebor represents a U.S. regulatory experiment, other jurisdictions are developing their own approaches to digital banking and crypto-friendly regulation. Singapore, Switzerland, and the United Kingdom have established frameworks that may attract fintech companies seeking friendlier regulatory environments.

U.S. institutions must compete not only domestically but internationally for technology company customers. If U.S. regulation becomes too restrictive or unpredictable, companies may choose to establish international operations and banking relationships, potentially reducing U.S. regulatory influence over the sector.

Key Takeaways for Fintech Leaders

As Erebor Bank moves toward full operation, several lessons emerge for fintech executives, investors, and legal counsel:

Political dynamics matter. Regulatory approvals are not purely technical exercises but involve political considerations, particularly for innovative business models that challenge existing frameworks. Building relationships with policymakers and regulators, maintaining bipartisan support where possible, and managing reputational risks are essential components of fintech strategy.

Capital requirements reflect risk. The OCC's insistence on a 12% Tier 1 Leverage ratio for Erebor demonstrates that innovative business models will face higher capital requirements than traditional banks. Fintech companies pursuing charters should plan for substantial capital raises and expect regulators to impose conservative requirements.

Multiple approvals create complexity. The need for both OCC and FDIC approval, plus Federal Reserve membership, creates a complex, multi-agency process where success is not guaranteed even after receiving initial approvals. Companies should budget time and resources accordingly and avoid premature announcements about launching services.

Diversification protects against concentration risk. Both for banks and their clients, concentration in specific sectors or service lines creates vulnerability. The SVB lesson remains relevant: neither banks nor their customers should become overly dependent on single relationships or business lines.

Regulatory frameworks are evolving. Digital asset regulation remains in flux, with different agencies taking varying approaches. Successful fintech companies will stay engaged with regulatory developments, participate in comment processes, and adapt their compliance programs as standards evolve.

Technology innovation must be paired with banking fundamentals. While Erebor's founders bring impressive technology credentials, the success of the bank will depend on sound risk management, experienced banking professionals, and adherence to fundamental principles of liquidity management, capital adequacy, and credit quality.

Conclusion

Erebor Bank's conditional OCC approval marks a pivotal moment in the convergence of traditional banking and digital assets. Whether this development represents visionary innovation or regulatory capture remains to be seen, but its significance for the technology and financial services sectors is undeniable.

For fintech companies, Erebor offers the prospect of specialized banking services designed for modern technology businesses, particularly those engaged in cryptocurrency, artificial intelligence, and defense technology. The bank's willingness to provide crypto-collateralized lending, stablecoin operations, and lending against innovative assets could unlock new financing options for growing companies.

However, significant uncertainties remain. Erebor must still obtain FDIC insurance, satisfy all conditional requirements, and prove its business model in practice. Political controversy surrounding the approval may subject the bank to heightened scrutiny and could influence whether other similar charter applications succeed. The concentration of services in emerging technology sectors creates risks that could manifest if crypto markets or AI investment cool.

Legal and compliance professionals working with technology companies should monitor Erebor's progress closely. The conditions imposed on the bank, its operational practices once launched, and any regulatory challenges it faces will provide valuable insights into how digital asset banking will be regulated going forward.

For the broader financial services industry, Erebor's approval suggests that the Trump administration's OCC is willing to support innovation in banking, particularly where it involves digital assets and technology sector services. This regulatory posture may encourage additional charter applications and accelerate the transformation of banking services.

The ultimate success or failure of Erebor Bank will shape regulatory policy, competitive dynamics in tech banking, and the future of digital asset integration with traditional finance. Technology companies and investors should prepare for both opportunities and risks as this experiment unfolds.

As financial technology continues to evolve, one lesson remains constant: regulatory compliance, sound risk management, and strong banking fundamentals matter more than political connections or technological sophistication alone. The institutions that balance innovation with prudence will thrive regardless of regulatory shifts or political changes.

Need Legal Guidance for Your Fintech Company?

Contact FinTech Law today for a consultation.

The regulatory landscape for digital banking and cryptocurrency services is rapidly evolving. While banking charter applications require specialized banking law expertise, our team helps fintech companies, digital asset businesses, and technology startups navigate the complex legal landscape of financial technology, securities regulation, and regulatory compliance.

Whether you're building relationships with banks like Erebor, developing digital asset products, or need guidance on securities and compliance requirements, FinTech Law provides sophisticated legal counsel to help you succeed in this dynamic environment.

Book a consultation to discuss:

- Securities and regulatory compliance for fintech companies

- Digital asset and cryptocurrency legal frameworks

- SEC regulations and registered fund compliance

- Capital raising and corporate formation strategies

- Compliance programs for financial technology businesses

- Legal strategy for fintech startups and growing companies

About FinTech Law

Experts in corporate formation, private and registered funds, capital raising, SEC regulations, and everything in between.

As fintech evolves, so should you and your legal team. FinTech Law provides sophisticated legal guidance to financial technology companies, digital asset businesses, investment advisers, and technology startups navigating the complex intersection of securities regulation, corporate law, and financial technology innovation.

Disclaimer: This blog post is for informational purposes only and does not constitute legal advice. The information contained herein is based on publicly available sources and regulatory filings as of October 2025. Regulatory requirements and banking laws are subject to change. Companies should consult with qualified legal counsel before making decisions based on this information.