FinTech Law Focus: U.S. Lawmakers Dig into Tokenizing Securities as Trump Ties Muddy Waters

Key Takeaways

- On March 25, 2026, the House Financial Services Committee held a hearing titled "Tokenization and the Future of Securities: Modernizing Our Capital Markets" — the most significant congressional examination of tokenized securities to date.

- Bipartisan consensus emerged: tokenized securities are coming, and they need the same regulatory guardrails as traditional securities — not a lighter-touch framework.

- The hearing arrived one week after the SEC and CFTC issued their landmark joint interpretive release establishing a five-category token taxonomy. Both developments are part of the same legislative moment.

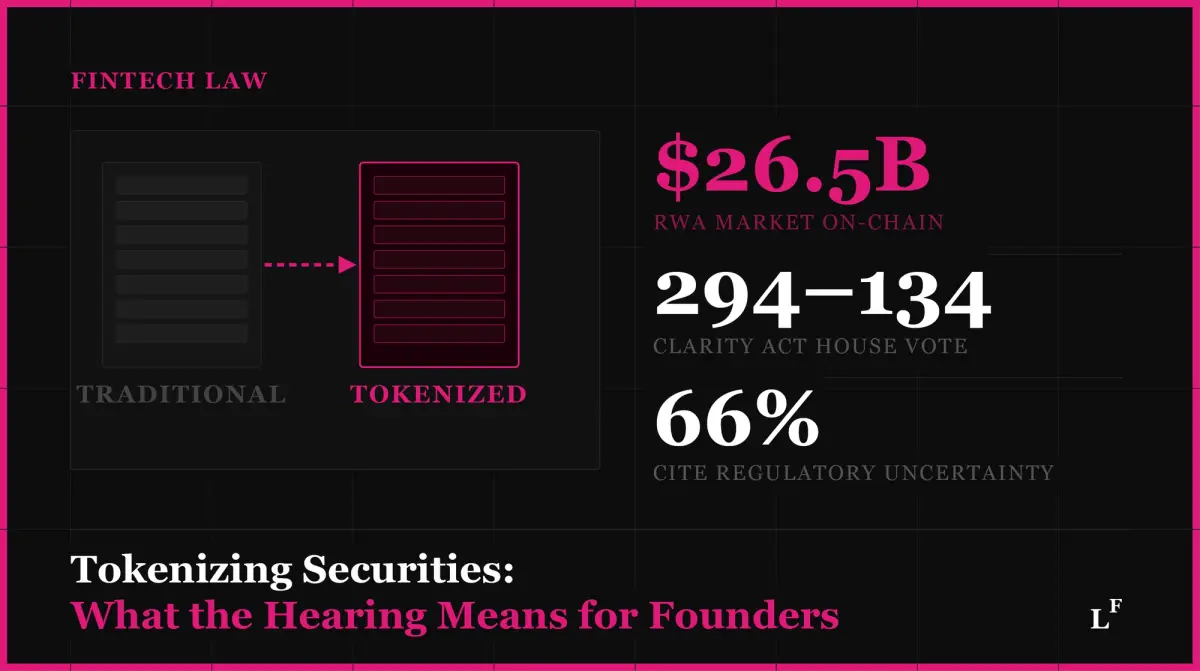

- The CLARITY Act — which passed the House 294–134 in July 2025 — is the most direct path to statutory codification. A Senate Banking Committee markup is targeted for late April.

- Unresolved questions remain around DeFi oversight, anonymous wallets, foreign ownership, and a 1982 tax law that may inadvertently penalize tokenized bond issuance.

- The tokenized real-world asset market has already reached $26.5 billion in distributed on-chain value. This is not a theoretical future. It is an incoming compliance reality.

What Happened

On March 25, 2026, the House Financial Services Committee convened a hearing titled "Tokenization and the Future of Securities: Modernizing Our Capital Markets." Chaired by Representative French Hill, the session examined how tokenization — the process of representing securities as digital tokens on a blockchain — intersects with existing U.S. securities law, and what new frameworks Congress may need to build.

The hearing arrived at an unusually consequential moment. Just one week earlier, the SEC and CFTC had jointly issued a comprehensive interpretive release establishing a five-category taxonomy for crypto assets under federal securities law (see our blog post on this topic). The CLARITY Act, which passed the House in July 2025 with a 294–134 bipartisan vote, is approaching Senate markup. And the tokenized real-world asset market has surpassed $26.5 billion in on-chain value as of late March 2026, growing at roughly 5–6% per month. (FinTech Weekly, March 23, 2026)

The Consensus: Same Asset, Same Rules

The most significant outcome of the hearing was not legislation — it was a bipartisan, on-the-record acknowledgment that tokenized securities are no longer a question of if, but when, and that the regulatory framework to govern them does not yet fully exist.

Across party lines, lawmakers and witnesses agreed on a foundational principle: tokenization does not change the fundamental nature of a security. A tokenized stock is still a stock. A tokenized bond is still a bond. The technology changes the infrastructure, not the investor protection requirements.

Securities Industry and Financial Markets Association (SIFMA) President and CEO Kenneth Bentsen framed it plainly: new entrants should face the same regulations and guardrails as businesses currently involved in stock trading. Blockchain Association CEO Summer Mersinger echoed the point, stating that "tokenization infrastructure will develop regardless" — the question is whether the U.S. regulatory framework will be ready when it does. Committee Chairman French Hill described tokenization as a structural transformation in how securities "are issued, traded, and recorded" at a foundational level — not a niche upgrade. (CoinDesk, March 25, 2026; DisruptionBanking, March 26, 2026)

Where the Parties Diverge

The bipartisan consensus on the principle did not extend to every detail. Democratic members raised concerns that went unresolved:

- Anonymous wallets and foreign ownership. The ability to transfer tokens peer-to-peer without a custodian raises KYC and AML compliance questions that existing broker-dealer frameworks do not fully answer. Ranking Member Maxine Waters flagged this directly.

- Gamification of trading. Waters also raised concerns that tokenization — by enabling faster, always-on trading with fewer friction points — could accelerate the gamification dynamics that equity trading apps have already introduced for retail investors.

- Trump family crypto ties. Democratic members raised the Trump administration's financial interests in digital asset businesses, including a stake in World Liberty Financial, as a conflict of interest framing the administration's pro-crypto regulatory posture.

These objections did not disrupt the core consensus on investor protection principles — but they signal that the political path to legislation involves more than technical agreement. (CoinDesk, March 25, 2026)

The Legislative Path: CLARITY Act and Two New Bills

Two draft bills were on the hearing agenda alongside the broader CLARITY Act discussion:

- The Modernizing Markets Through Tokenization Act of 2026 would require a joint SEC-CFTC study on tokenized derivatives — compelling both agencies to provide definitive answers on jurisdictional questions that have long been deferred.

- The Capital Markets Technology Modernization Act goes further, codifying the right of broker-dealers to use blockchain-based record-keeping under existing law.

Neither bill is law. But their presence signals that Congress has moved firmly past "is this real?" and into "what do we do about it?"

The CLARITY Act remains the central vehicle. If the Senate Banking Committee markup slips past late April, Senator Bernie Moreno has stated plainly that digital asset legislation may not move again for years — foreclosed by the midterm election cycle. (DisruptionBanking, March 26, 2026; FinTech Weekly, March 23, 2026)

An Unresolved Structural Risk: The 1982 Tax Problem

One of the most underreported issues raised at the hearing: a 1982 tax law — the Tax Equity and Fiscal Responsibility Act (TEFRA) — may inadvertently create severe penalties for tokenized bond issuance. Peer-to-peer token transfers are functionally indistinguishable from bearer bonds under TEFRA's current language, triggering potential denial of interest deductions, excise taxes at issuance, reclassification of capital gains, and a 30% withholding tax on interest. The global bond market represents over $100 trillion in outstanding debt, approximately $58.2 trillion of which is U.S.-based. If left unaddressed, this legacy provision could constrain tokenized bond issuance precisely when institutional demand for it is accelerating. (FinTech Weekly, March 25, 2026)

What This Means for Fintech Founders

The hearing did not produce new law. What it produced is something more foundational: a documented, bipartisan record that the existing framework is insufficient for tokenized markets, and that Congress is now actively working to change it.

For founders building tokenization platforms, digital asset infrastructure, or products that touch securities — the window to engage with the regulatory process is now. Comment periods, Senate markup hearings, and agency rulemaking notices are the venues where the framework gets built. Founders who participate shape the rules they will later operate under.

For founders whose products are adjacent to tokenized assets — compliance platforms, KYC tools, legal tech, custody solutions — the hearing signals a significant expansion of addressable market as institutional adoption of tokenization accelerates under a clearer legal framework.

Need help assessing how the emerging tokenization framework applies to your product? Contact FinTech Law for a consultation.

Disclaimer: This content is provided for general informational purposes only and does not constitute legal advice. The information contained herein reflects publicly available information and general legal commentary as of the date of publication. Regulatory frameworks governing digital assets and tokenized securities are subject to rapid change. Fintech founders and businesses should consult with qualified legal counsel regarding their specific circumstances before making any compliance or business decisions. FinTech Law LLC does not guarantee the accuracy, completeness, or timeliness of any information contained in this post.